Safeguard Your Equity Worldwide

News

Finance, HR & Legal: The Golden Triangle of Equity Management - And Why Only AI-Native Platforms Can Finally Close It

Finance, HR, and Legal all own part of equity management. Learn how AI-native platforms connect these teams to automate workflows, reduce compliance risk, and eliminate manual coordination.

Product

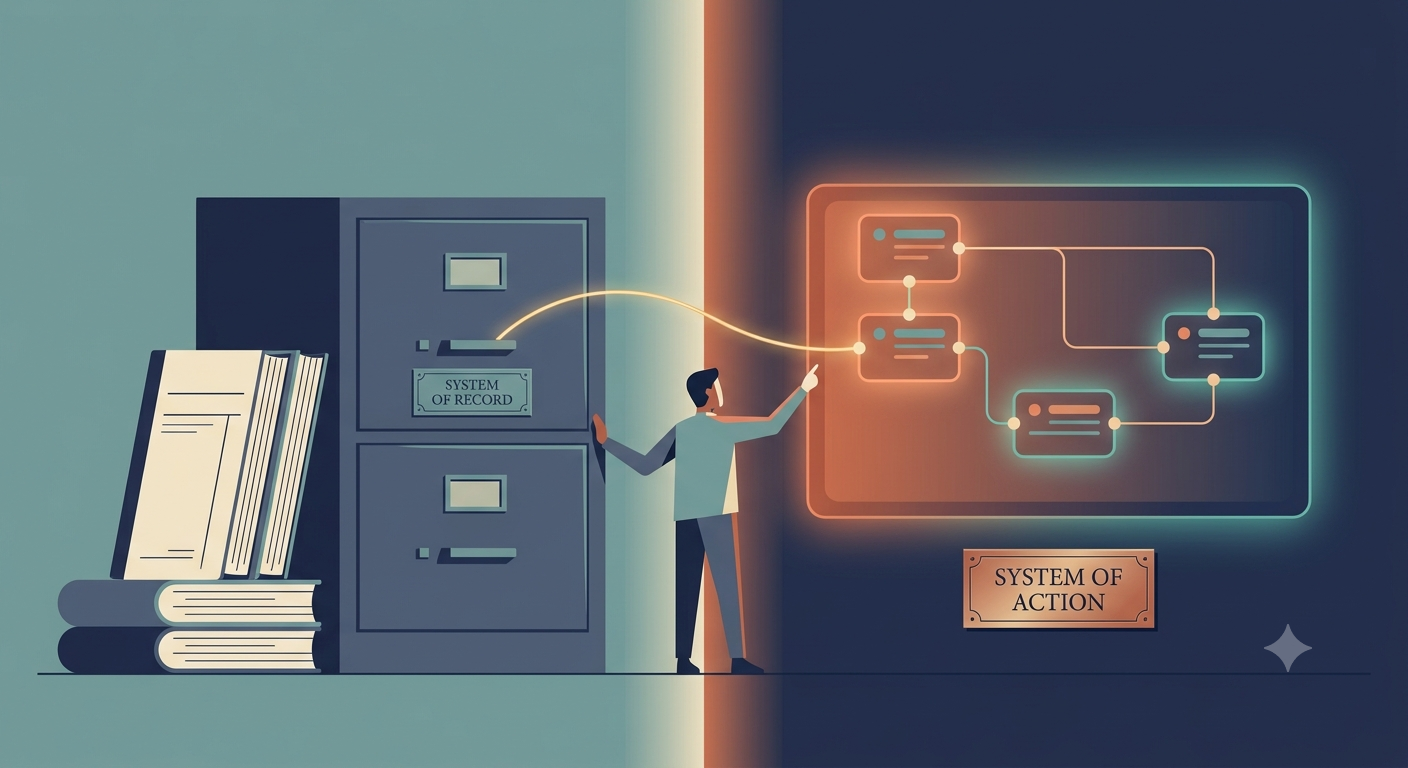

From System of Record to System of Action

Equity platforms were built to remember. Slice is built to act. Here's why a native AI agent - with the platform's data, permissions, and UI inside it - changes what equity software is.

.png)

News

What Does "AI-Native" Actually Mean in Equity Management?

Every equity platform says "AI" now. Here's what an AI-native equity agent actually does in practice - five real capabilities, live today.

Product

AI That's Built In, Not One You Plug In

Your security concerns about AI and equity data are valid. Here's why a built-in agent - not a connected chat tool - is the only architecture that actually holds up.

.png)

News

Australia's ESS Reporting Deadlines: What Employers Need to Know for July 14 and August 14

Australia's ESS reporting regime requires employee statements by July 14 and an ATO annual report by August 14. Here's what triggers a reportable event and how to prepare in time.

.jpg)

News

Equity Just Became Part of the People Platform: Slice + HiBob

Slice and HiBob have partnered to connect workforce data with global equity management, automatically syncing people changes into compliant equity workflows.

News

Finance, HR & Legal: The Golden Triangle of Equity Management - And Why Only AI-Native Platforms Can Finally Close It

Finance, HR, and Legal all own part of equity management. Learn how AI-native platforms connect these teams to automate workflows, reduce compliance risk, and eliminate manual coordination.

UK

UK ERS Filing: What Every Company With a UK Share Scheme Needs to Know Before 6 July, 2026

Learn what counts as a reportable ERS event, why nil returns are still required, and the risks of missing HMRC’s annual filing deadline for CSOP, EMI, and other UK share schemes.

Product

What Happens to Equity When Employees Move Countries

When an employee moves countries while holding unvested equity, the taxable income generally gets split between both countries based on where they actually worked during the vesting period

Product

Months of Legal Work, Millions in Fees: How Companies Used to Grant Equity Across Borders

The story of how one company managed global equity grants the old way, what it cost, and how Slice Global changed the equation with AI-powered compliance automation.

.png)

Product

Vesting Schedules Explained for Private Companies

Learn how vesting schedules impact equity, tax, and retention. Explore cliffs, RSUs, performance vesting, and compliance risks for private companies.

.png)

Product

AI-Native Equity Management: The Difference Between Infrastructure and Hype

Slice is the first AI-native global equity management platform. SliceAI is embedded into the infrastructure of the system rather than layered on top.

.jpg)

Product

Slice Global Raises $25M Series A to Build AI-Native Infrastructure for Global Equity Management

We’re excited to share that Slice Global has raised $25M in Series A funding, led by Insight Partners, with continued support from TLV Partners, R-Squared Ventures, and Jibe Ventures.

.svg)